The latest Liv-ex market update highlights a more structural – shift: the growing prominence of US wines within the secondary market itself.

Rising value, shifting demand: US wines on the secondary market

Much of the past year’s commentary has focused on how tariffs have shaped US demand for European wines. However, the latest Liv-ex market update highlights a different – and more structural – shift: the growing prominence of US wines within the secondary market itself.

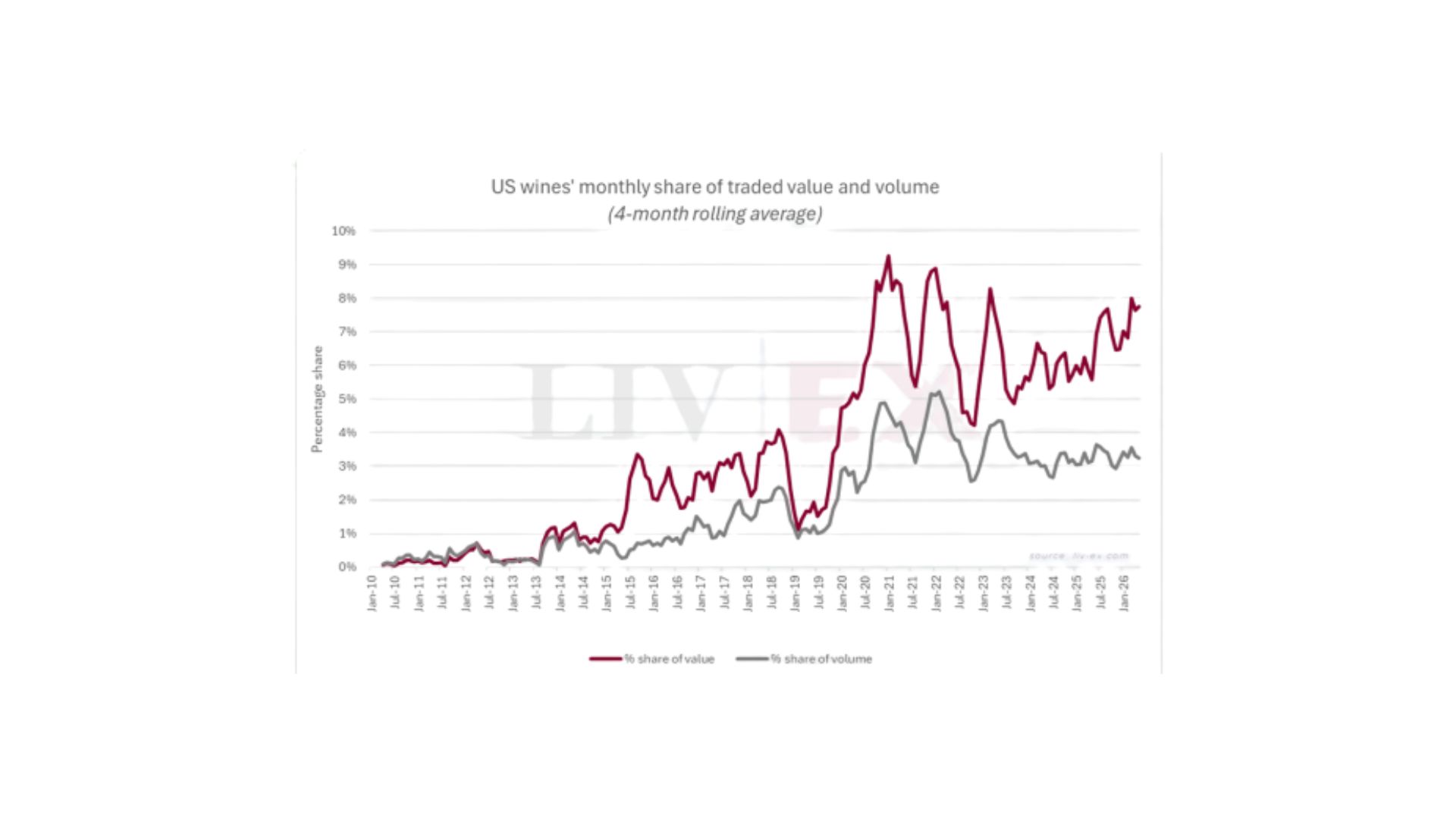

Data from Liv-ex shows that buyers are allocating a greater share of their spend to US wines than at any point over the past decade. While these wines accounted for less than 1% of trade on the platform ten years ago, they now represent more than 8%. For producers – particularly those in Napa Valley – this marks a meaningful change in how their wines are valued and traded internationally.

Liv-ex is the exchange for fine wine, market data and insight, providing a unique lens on secondary market behaviour. Crucially, wines listed on the platform must demonstrate resale value, meaning this growth reflects rising confidence in the investment and collectability credentials of US fine wine, rather than primary market supply.

The increase is overwhelmingly driven by Californian wines. While there is some representation from Oregon and Washington, activity remains concentrated in Napa and its leading producers.

The below graph compares the value of US wines traded (bought) on the platform, versus the volume. It shows that the value has increased more sharply than the volume. Demonstrating that people aren’t simply buying more (volume), they are spending more on US wines.

It’s also not the case that US wines are getting more expensive – Liv-ex tracks the price performance of the 50 most traded California wines. This data shows that buyers are opting for more expensive wines. This is thanks, in no small part, to Screaming Eagle, which makes up an increasingly high proportion of US wine trade.

Who is buying US wines?

The geographic profile of demand has also evolved. Prior to 2015, UK buyers dominated the secondary market for US wines. Since then, their share has declined as participation from European and Asian buyers has expanded.

“US buyers’ purchasing of US wines is notable. We might imagine that for US buyers it would be cheaper to acquire wine domestically. For those without initial allocations, this appears not to be entirely the case. US buyers’ increasing share of purchasing prior to tariff impositions is not the sole contributor to their increased share. Rather, since the start of 2023, the percentage of their total purchasing allocated to US wine has been steadily rising.’’ – Sophia Gilmour, Market Analyst, Liv-ex

This suggests a broader, demand-led shift rather than a short-term reaction to policy changes.

Conclusion

The growing share of US wines on the secondary market reflects a structural evolution. Increased participation from international buyers, combined with a clear tilt towards higher-value bottles, indicates that US fine wine is consolidating its position within the global fine wine market.

While activity remains concentrated among a relatively small group of benchmark producers, the direction of travel is clear: US wines are no longer marginal on the secondary market. Instead, they are becoming an increasingly established component of global fine wine portfolios.

About Liv-ex

Founded in 2000, Liv-ex is the global exchange for the fine wine trade, providing market data and insight. Headquartered in the UK with operations in France and Belgium, Liv-ex connects more than 550 businesses across 42 countries through its trading platform.

Facts Only

* Buyers allocate a greater share of their spend to US wines than at any point over the past decade.

* US wines accounted for less than 1% of trade on the platform ten years ago, now representing more than 8%.

* The increase in value has increased more sharply than the volume traded.

* The growth is concentrated among Californian wines, specifically Napa Valley producers.

* Prices reflect an option for buyers to opt for more expensive wines, including those like Screaming Eagle.

* Buyer geographic profile evolved: UK buyers dominated US wine secondary market prior to 2015.

* Since 2015, participation has expanded from European and Asian buyers.

* US buyers' increasing share of purchasing rose steadily since the start of 2023.

* Wines listed on Liv-ex must demonstrate resale value.

Executive Summary

Full Take

Sentinel — Likely Human

This article reads like a well-structured synthesis designed to interpret market data rather than raw reporting, exhibiting characteristics consistent with AI-assisted analysis or high-level wire copy.