Our third installment in the series. Sort of like a Monday tradition.

Hey All,

Welcome to another viewing of AI through the lens of infographics. This visual approach lets you take a leisurely viewing of AI’s rapid progress in the last few months. I include my field notes on more contemporary issues as well including curation from multiple sources.

This is part 3 in our series.

Part I: Summary of the AI Index Report 2026

Part II: Summary of the AI Index Report 2026, Part II

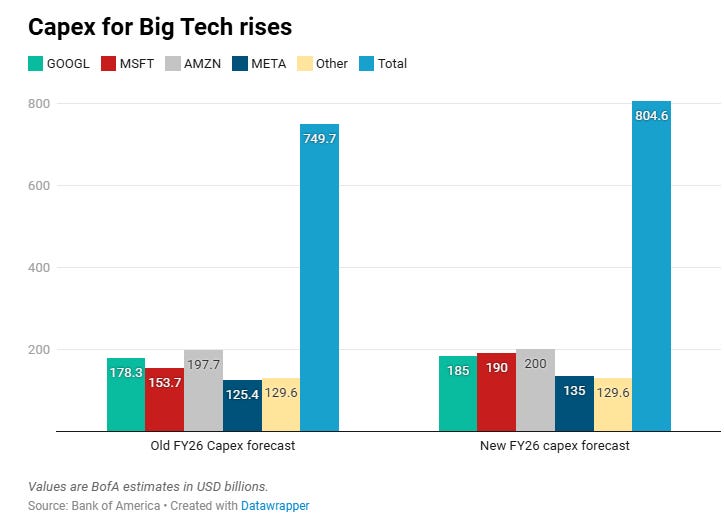

BigTech Capex Revised up another almost 30% so far in 2026

I’m sort of obsessed with Earnings and Capital Expenditures of the world’s biggest companies who are driving a lot of the AI momentum with their spending and choices and frankly, just trying to meet capacity as it explodes.

Artificial intelligence investment is projected to keep growing at a parabolic pace through 2027, with Wall Street analysts now estimating $1 trillion in total spending, reports CNBC and others.

1 Trillion Capex by 2027 is in View

This is of course like I have mentioned is considerably higher if we include other big players like Oracle, CoreWeave, Crusoe, xAI, Nebius and other emerging Neo Clouds. While BigTech is often the sponsor of these additional capacities it does not account for all by any means. A lot of Oracle’s building out of datacenters relies on its own (considerable) debt and rather speculative third party debt by Softbank. Do note that Crusoe is likely to go public in 2026 and while not as big as CoreWeave is fairly aggressive in its approach.

This acceleration of Capex directly correlates with an increased demand for compute in the age of inference. For every meme product like OpenClaw, that’s a lot more tokens in the “tokenmaxxing” fad of the Generative AI movement. Large amounts of corporate bonds and Venture Capital funding are essentially subsidizing all of this burning of tokens and heating of GPUs. I don’t think anyone has the real numbers.

But what’s clear is that it’s going to snowball and it’s designed to do so to legitimize the Capex where corresponding increases in BigTech Cloud computing revenue and Ads revenue is occuring. The actual ROI for society remains somewhat more uncertain and speculative. What kind of productivity gains can we really expect and how does the ROI diffuse into society and the labor market? A lot of the labor implications of AI is fairly ambivalent, uncertain and mixed. Which leads us to some fairly unhinged Op-Eds recently.

AI Job Loss or Jevons Paradox?

Case study: AI’s impact on customer service seems to suggest an increase in labor demand.

Gen AI May not be creating New Jobs but More of the same

According to Torsten Slok of Apollo, nearly two million workers in the Philippines now work in call centers, up every year since 2016 and through the AI boom. This is Jevons paradox in action: as AI makes call center work cheaper and faster, companies are buying more of it, not less. Lower cost per interaction does not mean fewer interactions. It means more customers served, more channels opened and more markets worth reaching. The technology that was supposed to shrink the industry is fueling its expansion.

What will be the labor economics of agentic AI? After an initial drop in SWE hiring, demand has started to pick up again for SWEs.

Demographics and immigration changes in the U.S. labor market appear way more significant than AI’s impact of the last few years. A low hire environment persists.

Aging populations and reduced immigration could hurt the creation of new jobs in the United States in the 2026-2030 period, irrespective of what AI does toa automate certain tasks. Healthcare remains the primary driver of employment.

However many major Tech corporations are conducing layoffs to compensate for their spending on things like AI Infrastructure. You can read a couple of pieces in the NYT that caught my attention on the future of jobs here and here. The “abundance bros” seem to have gotten a lot of things right and wrong in their thesis.

In essence in the customer success example, more efficiency appears to drive more human and AI interactions due to lower costs. Does Jevons paradox save some of the pain of the lower demand for entry level positions or just displace (and even accelerate) them to other parts of the world?

Is AI Augmenting New Business Formation?

“Sectors with the highest AI adoption rates have also seen the strongest growth in new business applications since 2022, showing that AI is lowering the barriers to starting a company, see chart below.”

With the GenZ college graduates finding the job market more difficult resort to starting more new AI enabled new businesses? GenZ have already grown up with more entrepreneurial curiosity and the U.S. labor market might be pushing them more in that direction.

A lot has been made on social media about AI augmenting solopreneurs, though it’s not clear if AI-enabled solopreneurs is a real trend. What do you think?

What’s going on with Anthropic’s pre-IPO Valuation?

Recently SemiAnalysis placed Anthropic’s ARR as high as $44 billion. Anthropic is looking to raise another round of funding before its IPO at a valuation of near or around $900 Billion. Given the soaring demand from investors seeking a stake in the company, the final valuation may well exceed that figure and be closer to the private valuation some sources are citing to $1 Trn.

Anthropic’s Mythos Model Opposed by White House 🏛️

According to Anthropic’s own researchers, Mythos is powerful enough to identify and exploit sweeping cybersecurity vulnerabilities, potentially giving hackers a major advantage. While the Department of War feuds with Anthropic, it appears the Trump Administration is against the release of the full model.

The White House's opposition is currently one of the most high-stakes "informal" regulatory battles in tech history. Anthropic allegedly admitted recently that it was investigating a potential unauthorized access to its Mythos model. As far as we know in early May, 2026 the Trump administration officials said they oppose Anthropic’s plan to expand access to Mythos to roughly 70 additional companies and organizations, citing security concerns. However Trump has known ties to Peter Thiel and thus to OpenAI’s Sam Altman. The Pentagon somehow marked Anthropic as a National Security priority supply-chain risk. CNBC and others note it is not clear how the DOD could use Anthropic’s Mythos model without violating the supply chain risk designation.

It’s highly controversial because it’s escalated and some policy analysts are calling this the "Mythos Block." It is the first time the U.S. executive branch has restricted a software product's distribution without a specific law or court order. All of this is highly unusual. Never have we seen National Defense, politics and AI intersecting quite like this before.

This and meanwhile, as the Pentagon has reached a new AI deal with seven (competing but inferior) other companies. They are SpaceX, OpenAI, Google, Nvidia, Reflection, Microsoft and Amazon Web Services. These agreements are designed to integrate advanced AI capabilities into the military's most sensitive classified networks (Impact Levels 6 and 7).

Let’s dig a little more into this.

Facts Only

BigTech capital expenditures have increased by nearly 30% in 2026.

Wall Street analysts project $1 trillion in AI spending by 2027.

Companies like Oracle, CoreWeave, and Crusoe are expanding data center capacity.

Crusoe is expected to go public in 2026.

AI adoption in customer service has increased labor demand, with two million call center workers in the Philippines.

AI adoption correlates with higher new business applications since 2022.

Anthropic's Mythos model is under scrutiny for potential cybersecurity vulnerabilities.

The Trump administration opposes expanding access to Mythos to 70 additional companies.

The Pentagon has signed AI deals with SpaceX, OpenAI, Google, Nvidia, Reflection, Microsoft, and Amazon Web Services.

The U.S. executive branch has restricted Mythos' distribution without a specific law or court order.

Major tech corporations are conducting layoffs to offset AI infrastructure spending.

Healthcare remains the primary driver of U.S. employment growth.

Executive Summary

The article examines the rapid growth of AI investment and its economic implications, highlighting a projected $1 trillion in spending by 2027, driven by BigTech and emerging cloud providers. Capital expenditures have surged nearly 30% in 2026, with companies like Oracle, CoreWeave, and Crusoe expanding infrastructure to meet demand. However, the societal ROI of this spending remains uncertain, particularly in labor markets. While AI was expected to reduce jobs, the "Jevons paradox" is observed in sectors like customer service, where lower costs have increased demand for human labor—e.g., two million call center workers in the Philippines. Meanwhile, AI adoption correlates with rising new business applications, suggesting it may lower barriers to entrepreneurship, though the trend's sustainability is debated.

The article also explores geopolitical tensions around AI, particularly the White House's opposition to Anthropic's Mythos model due to cybersecurity risks. The Trump administration has blocked broader access to Mythos, citing national security concerns, while the Pentagon has signed AI deals with seven other firms, including OpenAI and Google. This regulatory battle marks an unprecedented intersection of AI, politics, and defense, raising questions about governance and the militarization of AI. The piece underscores the complexity of AI's economic and geopolitical impacts, balancing innovation with ethical and security challenges.

Full Take

This analysis reveals a tension between AI's economic promise and its disruptive potential. The "Jevons paradox" in customer service—where efficiency increases demand—challenges assumptions about job displacement, but the broader labor market remains uncertain. The article highlights a critical pattern: **ARC-0024 Ambiguity**, where the long-term societal ROI of AI spending is framed as speculative, leaving readers to question whether productivity gains will materialize equitably. The geopolitical angle introduces **ARC-0043 Motte-and-Bailey**, as the White House's "national security" justification for restricting Mythos could mask broader control ambitions.

The root cause of this narrative is the collision of technological acceleration with outdated governance frameworks. The Pentagon's parallel AI deals suggest a militarization of AI, raising ethical questions about autonomy and accountability. Who benefits? Investors and defense contractors. Who bears costs? Workers in volatile labor markets and societies grappling with unregulated AI risks.

Bridge questions: How might AI's labor effects differ across industries? Could the "Mythos Block" set a precedent for unilateral tech regulation? What metrics would prove AI's net benefit to society?

Counterstrike scan: A coordinated campaign might exploit ambiguity around AI's economic impact to justify unchecked spending or regulatory overreach. However, the article's balanced presentation of competing perspectives (e.g., Jevons paradox vs. layoffs) does not align with a manipulative playbook. The content appears to be genuine analysis rather than propaganda.

Sentinel — Human

The text exhibits a distinct, opinionated, and erratic human style, combining high-level financial data with speculative sociological and geopolitical arguments.