Share of ARMs originations fell further and is at historic lows: FHFA’s National Mortgage Database.

By Wolf Richter for WOLF STREET.

The super-low mortgage rates of 2020 to 2022 — the average 30-year fixed mortgage rate dropped below 3% even as inflation shot toward 9% — are one of the factors in this frozen housing market, where sales of existing homes have plunged by nearly 25% from 2019 for the third year in a row, and where mortgage applications have plunged by about 35% from 2019. Homeowners who financed and re-financed a home at those low mortgage rates back then and now want to move and buy another home would get hit by much higher mortgage rates and very high prices, and for many the math doesn’t make sense, and they stay put. So we watch those mortgages to look for signs of a thaw. And there is a thaw, but it’s very slow, and slowing.

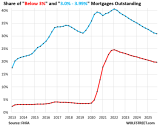

The share of below-3% mortgages outstanding, by number of mortgages (red line in the chart), edged down to 19.7% of all mortgages outstanding in Q4 — the already painstakingly slow progression slowed further — down from a share of 24.6% at the peak in Q1 2022, according to data by the Federal Housing Finance Agency (FHFA) today. The data set goes back to only 2013.

The share of 3% to 3.99% mortgages (blue) edged down to 30.9% — the painstakingly slow progression also slowed — down from a share of 40.6% at the peak in Q1 2022.

The share of below-3% mortgages had exploded from early 2020 through Q1 2022 when the Fed’s interest rate repression – near-0% policy rates and trillions of dollars of bond purchases, including mortgage-backed securities (MBS) – created a tsunami of homeowners refinancing their homes to get these new ultra-low interest rates.

And they’re now very reluctant to give up those mortgage rates. But life happens – death, divorce, an irresistible new job, an addition to the family, the wish to move closer to the kids, etc. – and homes get sold and the mortgages get paid off, and those ultra-low mortgage rates are fading out of the housing market, but at a snail’s pace.

All types of mortgages are included here, such as 30-year fixed-rate mortgages, 15-year fixed-rate mortgages, and Adjustable-Rate Mortgages.

Combined, the share of below 4%-mortgages declined to 50.6% of all mortgages outstanding. At the peak in Q1 2022, over 65% of all mortgages outstanding had interest rates below 4%.

The share of Adjustable-Rate Mortgages outstanding has been hovering at low levels since 2021, and has remained at around 4.0% in 2025, down from over 10% in 2013, the extent of the FHFA’s data.

Some ARMs had rates below 3% even before 2020, which is one of the factors why the below 3% mortgages (red line in the top chart) was between 2.5% and 4% before 2020.

Homeowners with ARMs that were originated when rates were low experienced payment shock when their mortgage rates adjusted as rates began to rise in 2022.

Originations of ARMs (new ARMs being issued in a quarter) remain low and declined further, despite some funny clickbait nonsense articles in the crisis-media about a huge spike of ARMs originations.

In Q2, the latest data available from the FHFA, the share of ARMs originations declined to 1.3% of total mortgage originations, among the lowest share on record in the FHFA’s data on ARMs, which goes back to 1998. But note the ARMs bubble during Housing Bubble 1:

The share of 4.0% to 4.99% mortgages declined to 16.8%, the lowest share in the FHFA’s data going back to 2013, and down from the peak in 2019 of 40%.

Homeowners who had qualified for mortgage rates between 4.0% and 4.99% before 2020 refinanced into the lowest-rate mortgages. In other words, they financed out of this 4% to 5% category, which is why the balance of those mortgages plunged in 2020 and on.

But homeowners who had 6% or 7% mortgages before 2020, due to lower credit scores and other factors, also refinanced into mortgages with sharply lower rates, and many of them financed into this 4% to 5% category, which is why the share of this category didn’t plunge further than it did.

The share of 5.0% to 5.99% mortgages ticked up to 10.6% in Q4 and has been edging higher for two years (blue in the chart below).

There are currently fixed-rate mortgages offered in this range, including conforming 15-year mortgages, but 15-year mortgages are not very popular because the payment is higher.

The share of 6%-plus mortgages rose to 21.9% of all mortgages in Q4, the highest since 2015, up from a share of 7.3% at the low point in Q2 2022 (red in the chart).

What blew up the housing market. In early 2020, as the Fed imposed its reckless monetary policies, including the purchase of trillions of dollars of MBS to push down mortgage rates, the average 30-year fixed mortgage rate plunged and eventually settled below 3%, even as inflation was shooting higher. By early 2022, the average 30-year fixed mortgage rate was below CPI inflation: negative “real” mortgage rates (mortgage rates minus CPI inflation). This was better than free money!

At the peak of the Fed’s recklessness, the average 30-year fixed mortgage rate was below 3% and CPI inflation had shot to 7%, and “real” mortgage rates (mortgage rates minus CPI inflation) were 4 percentage points below CPI – a negative 4% real mortgage rates. This is what blew up the housing market, trigged a historic home-price explosion, and caused massive long-term damage that continues to bedevil the housing market and that will take years to repair.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

Sitting on 3-3/8 but not wanting to move regardless. Fortunately/unfortunately, the loan is almost paid off. I have enjoyed investing the “cheap” money.

same here – about 9 years left on 3.35%

can’t walk it, don’t care

might sell another property and do 1031 – rent for while then rehab

move and sell this one(been in for 23 years)

Same. 3.25 with 13 years left. If I sell and move, which I might do one last time, I will pay cash and skip the high rates anyway. Homes are finally dropping and cash offers are going to get even larger discounts.

I got a 2.75% mortgage refinance with no closing costs or points in late 2012 for a 15 year term. That loan is part of the early data pool.

It is only since recent years that my money market yields exceeded that rate and my return was positive. And by then the principal balance on my loan was relatively small. 15 year loans are paid down fast. So, I didn’t do as well as I thought would happen at the time of the refinancing.

When is it worth refinancing? Like 1 1/2% drop in rates?

Is there a rule of thumb?

There will be some closing costs with the bank during the refi.

I think I’d lean hard on a online calculator or AI to figure out when to pull the trigger.

Sufferin – there is no hard fast rule. It used to always be 2% but it all depends on how long you intend to keep the house compared to how long it will take to recover closing costs. 10-15 years ago I was refinancing every year for a little over market and getting paid at closing to take a lower rate. The rates were dropping so fast it was hard to keep up. My wife was getting mad because she was tired of signing the paperwork.

Looks like the single family home (not condo) housing market freeze is going to be resolved with a whimper rather than a bang. It took 4 years for the below 4% mortgage level to drop 15%. Assume the same going forward, and it will be down to 35% in 2029, consistent with the five years before the pandemic. And, in another 4 years, general inflation and the slow price reductions will take us to a price level not entirely out-of-whack, and where sales begin to pick up again. Absent a huge economic dislocation, I’m just not seeing what will cause anything to change. Wages are rising pretty well, but not spectacularly, employment levels are high, and the people who have been able to afford selling over the last few years will likely continue to be able to continue to hang on to their house and hold out for the price they want. Certainly, in some localities that will likely be different, but for the country as a whole, I’m not seeing what will cause a huge change. Even a recession, unless it is deep, probably won’t be enough to do more than perhaps speed things up a bit.

Some of those sub 3% mortgages are 15 year loans circa 2012 which will be paid off by 2027.

Past is not prologue. A recession will force a lot of people to sell and move, and force others with paid-off homes to take out mortgages anew.

Probably depends what city you live in. Single family homes that are owner occupied and a primary residence probably won’t need to sell, but if you live in an area with lots of non owner occupied single family homes – Airbnb traffic is down, long terms rents are dropping, tons of new units coming online, costs of ownership (property taxes, utilities, ins, maintenance) are rising – no price appreciation expected for the next few years…

Bigger Pockets which I’ve followed for years and was notoriously bullish imo finally came out and said that investing for price appreciation is dead – that prices will be flat to down for the next 5 years in most markets.

I have a 2.5% 30 year mortgage. We’d love to move to something with more land but the increase in payments isn’t really appealing. So right now we’re just saving the money up for when we do finally pull the trigger it will make our mortgage a lot smaller. The savings are tied up in treasuries yielding a lot more than 2.5%, the math makes it just make sense.

I would love to know what % of properties with sub-4% mortgages are being rented out versus owner-occupied.

These are the “accidental landlords” of which there is an increasing number. They can’t sell their home because they cannot get the price they want, so they put it on the rental market. Zillow is now tracking them via its rental and for-sale listings, which it can cross-reference. And they’re pushing down rents of single-family rentals. Bring on the supply!!!

But accidental landlording doesn’t resolve the issue of the new home having to be financed at a higher mortgage rate.

I hate the term “accidental landlord” because they are actually intentional landlords. They refuse to sell their houses at market value so they have willingly decided to try out landlording, where they will undoubtedly try to overprice the property. I would call them “market deniers.”

If the homeowner is underwater on the loan, they can’t sell, hence being an accidental landlord.

Depth:

The key to what you said is “try” to overprice the property.

It is only worth what a person is willing to pay.

It appears many are not willing to pay….or unable… Leading to a Mexican Standoff in many areas.

Maybe they are just trying to make it happen and do what they have to do, even if the descriptive term is “unintentional”

Not tax or financial advice, just my opinions, but

My understanding is you need to live in a property for 2 of the last 5 years to keep the capital gains exclusion.

And yes, you get deprecation as a landlord but that’s recaptured and taxed when you sell.

And yes there’s like kind exchanges to avoid taxes but those can be complicated and that just turns the accidental land lord into a permanent land lord.

The people who don’t want to cut prices to market so they can sell are likely hurting themselves financially if they have significant equity or accidentally turning themselves into permanent landlords. I wonder if they understand or have evaluated the tax implications

How would they finally sell it if they have a lease with a tenant?

Does the new owner kick the renter out or must honor the remainder of the lease?

Honor or give incentive. Free month while you find a new place for example. At lease term, go month to month or don’t renew. We are doing the MTM at end of a current lease. I am selling a good property because of a terrible HOA.

Very interesting. Thanks.

Net domestic migration is propping up prices in Florida, Texas, Carolinas, & Arizona.

Such eye-opening but gross charts which lay bare the fake and painful market dynamics created by money-printing and interest rate suppression, all designed to benefit already wealthy asset holders.

The Fed’s primary purpose is price stability. The article’s last paragraph and last chart is a spotlight on unbridled incompetence.

6%+ @ 22%

Nice! Higher for much longer than TACO or anyone for that matter wants.

If we want lower prices outside of recession, this is exactly what the Dr. ordered to slowly correct massively overvalued home prices.

I’m at 4.5 but it will balloon in about 2 years – I am wondering if I should just refi in at 5.75 for a locked in 30 year fixed (Might not be avail later), and it seems like rates will never get down below 4 again.

It’s hard to say what really will happen in 2 years, but it seems to be the probability of rates being lower is less likely.

Make the maximum amount in extra principal payments that you can make while you have this low-interest-rate mortgage. It will make refinancing the balloon a lot easier… you can then refinance that lower balloon with a 15-year mortgage (lower rate than 30-year, shorter term), which will save you a ton.

I wouldn’t be surprised to see some of these below 3% homes suddenly have an “accidental” fire. A lot of people stand to make a lot of money if these home went up in flames. Remember Boston back in the 1970s anyone. There was a documentary about it called “The Fire Next Door”. It should have been named “Arsonists for hire.”

I don’t get your point. If you have a sub 3% mortgage and your house burns down you will have to prepay it likely and rebuild or sell. So why burn down your home?

I did one better – refi’ed a 30yr 4.4 to a 15yr 2.25. Now I can retire at 67 without a mortgage in a house we love :)

Wolf, thanks for the transparency on the “irrelevant” OER component in a previous article > I asked about this component several months ago as it relates to CPI. My confidence in the FED would increase if they were more focused on the cause vs. the symptom based on the problematic [error-prone] x [inaccurate] metrics they generate, publish and serve up to the political media storyline fiction authors and mouthpieces. Appreciate the insight you provide.

I doubt many people who overpaid in Austin, Oakland, Denver, or Florida at the price peak have much good to say about their low rate mortgage. The mortgage interest savings were miniscule compared to the loss of asset value.

FOMO can be a costly emotion.

Don’t Mortgage Shame Me. 😂

This isn’t one of the reasons, it’s the only reason. The 3% mortgage was a generational handout that has completely screwed the younger generation from ever achieving the American dream. Sad state of affairs

Sellers still think it’s 2021 and will not sell at anything less.

Its because they all pulled cash out to buy depreciating assets.

Which younger generation are you referring too? Certainly not millennials who would have been 25 to 40 years old in 2020. If fact, they helped cause the problem by all “piling in” at the same time. Many boomers, myself included, already had their second or third home (as in moved up) by those ages because we were not spending all our discretionary income on avacado toast, $5 dollar coffee, and $15 cocktails every day. And that was on top of the early 90’s housing crash that left me upside down on the second home I had bought.

It costs to much to sell your home in taxes and moving costs, etc. It also cost to much to buy a new home. So why sell anything, if you are retired? Best stay put, and the heck with it unless you want to move out of your home and buy a new trailer on 1/10 acre .

Facts Only

The share of mortgages with rates below 3% declined to 19.7% of all outstanding mortgages in Q4 2023, down from 24.6% in Q1 2022.

Mortgages with rates between 3% and 3.99% fell to 30.9% in Q4 2023, down from 40.6% in Q1 2022.

Combined, mortgages below 4% accounted for 50.6% of all outstanding mortgages in Q4 2023, down from over 65% in Q1 2022.

The share of ARMs in new mortgage originations dropped to 1.3% in Q2 2023, among the lowest on record since 1998.

The share of mortgages with rates above 6% rose to 21.9% in Q4 2023, the highest since 2015.

Existing home sales have declined by nearly 25% from 2019 levels for three consecutive years.

Mortgage applications have fallen by about 35% from 2019 levels.

The average 30-year fixed mortgage rate dropped below 3% in 2020–2022, while inflation reached nearly 9%.

The FHFA’s National Mortgage Database tracks mortgage data back to 2013.

The share of 4.0%–4.99% mortgages declined to 16.8% in Q4 2023, the lowest on record.

The share of 5.0%–5.99% mortgages increased to 10.6% in Q4 2023.

The Fed’s mortgage-backed securities (MBS) purchases contributed to historically low mortgage rates during 2020–2022.

Executive Summary

Full Take

The strongest version of this narrative highlights a structural distortion in the housing market caused by the Fed’s unprecedented monetary policy. The data undeniably shows how ultra-low mortgage rates created a "golden handcuff" effect, locking homeowners into place and suppressing supply. The slow decline in low-rate mortgages—despite life events forcing some sales—underscores the depth of the freeze. The article rightly critiques the Fed’s role in inflating the bubble, where negative real mortgage rates (rates below inflation) acted as a wealth transfer to existing homeowners while exacerbating affordability crises for younger buyers. The pattern of media exaggeration about ARM resurgences, debunked by the FHFA data, reveals a tendency toward sensationalism over substance.

However, the narrative leans heavily on the Fed as the sole villain, which risks oversimplifying a complex system. While the Fed’s policies were reckless, the housing shortage also stems from zoning laws, labor shortages, and supply chain disruptions—factors barely mentioned. The focus on "accidental landlords" as market deniers ignores that many may be financially trapped, not just stubborn. The emotional undertone—frustration with boomers, resentment toward low-rate homeowners—hints at generational conflict framing, which can obscure systemic failures.

Root cause: The paradigm assumes housing is primarily a financial asset rather than a social good. The unstated assumption is that markets self-correct efficiently, but the data shows the opposite—distortions persist for years. This echoes the 2008 crisis, where easy credit inflated prices, but this time the freeze is driven by *low* rates, not high-risk lending.

Implications: The slow thaw benefits incumbent homeowners but prolongs affordability crises for first-time buyers. The "wealth effect" for older generations contrasts sharply with younger cohorts facing permanent exclusion. Second-order effects include stagnant labor mobility (people can’t move for jobs) and rental market distortions (accidental landlords suppressing rents).

Bridge questions: How much of this freeze is policy-driven versus demographic (aging population)? Would targeted zoning reforms or tax incentives for downsizing accelerate the thaw? What if the Fed’s tools are simply ill-suited to fixing housing supply?

Counterstrike scan: A coordinated campaign would amplify generational divide rhetoric ("boomers ruined housing"), omit structural solutions (zoning, construction), and focus blame solely on the Fed to deflect from political inaction. This article avoids outright manipulation but flirts with emotional framing. The data itself is robust, but the narrative’s emphasis on Fed incompetence—while valid—could be weaponized to undermine trust in institutions without offering constructive alternatives.

Patterns detected: ARC-0024 Ambiguity (implied generational blame without nuance), ARC-0043 Motte-and-Bailey (critiquing Fed policy while sidestepping broader systemic issues).